Olneyville is a neighborhood on the west side of Providence, Rhode Island. Once home to a thriving textile industry, the economy collapsed after World War II, and in subsequent decades it became one of the most distressed places in the state. In 1978 the Providence Planning Department found that over half of Olneyville’s houses needed “immediate attention,” were in a state of “advanced deterioration,” or were “heavily deteriorated and dilapidated.” Twenty years later, when downtown Providence was becoming what the New York Times called “a national model for how to make a run-down old city hot again,” Olneyville was suffering through stubbornly high levels of crime, unemployment, and despair.

Today, people reach for very different words to describe the neighborhood: hip, trendy, chic. In the 2000s, nonprofits converted a sprawling, toxic dump into a prize-winning park. A community development corporation replaced scores of vacant lots and abandoned buildings with below-market rate housing. School officials remade its local elementary school into a treasured neighborhood anchor. At the same time, these victories that low-income residents and their allies worked so hard to achieve brought the neighborhood to the attention of an entirely new demographic.

Between 2000 and 2015, average rents in Olneyvillle climbed over 54 percent, more than twice the city-wide average. Over roughly the same period the number of people in the neighborhood who had attended college nearly doubled, and the number with a college or advanced degree nearly tripled. From 2009 to 2018, the number of Non-Hispanic white residents in Olneyville increased nearly 60 percent, and the Gini Inequality Index, a standard measure of income inequality, increased more than 10 percent. In short, Olneyville has become whiter, significantly more unequal, and substantially more expensive, and gentrification now imperils the Latinx community that has called Olneyville home since the 1990s.

The lesson—one repeated time and again across the country—is that America’s current approach to neighborhood well-being can transform places like Olneyville but cannot protect them. This approach distributes meager pools of money from foundations, philanthropies, and anchor institutions like universities and hospitals, as well as very limited public-sector funding, to an eclectic array of chronically underfunded nonprofit organizations that act on behalf of distressed neighborhoods. The entire model is non-confrontational and technocratic, relying heavily on well-intentioned and well-credentialed outsiders to set the priorities, solicit the funding, and manage the work.

But low-income residents in neighborhoods like Olneyville don’t need their lives managed. They need a stream of funding that is adequate and secure, but not controlled by outsiders. They need connections to, and relationships with, people in power. They need a mechanism that decommodifies property so that capital cannot displace longtime residents and businesses. They need a tool that allows people in the neighborhood—rather than an outside organization—to capture increases in the value of land. And they need collective power to help ensure that as capital approaches, public institutions like schools and the police are aligned with the poor rather than the wealthy.

What they need is an innovation that I call a neighborhood trust.

A trust is simply a legal instrument that owns assets for the benefit of some other individual or group. The group could be a family or an organization, but it can also be the residents of a particular place, like a neighborhood. The assets can be anything of value, including land, buildings, cash, businesses, and other things in a neighborhood. These assets are overseen by a group of trustees, who manage and administer the trust pursuant to a set of rules that are established when the trust is created, and can be modified over time to meet the changing needs of the group. The trustees do not own the wealth; the trust owns the wealth for the group’s benefit. But the trustees oversee it according to rules designed to protect, preserve, and increase that wealth. Trustees are chosen or designated when the trust is created, and they can serve indefinitely or for a fixed term.

A couple of examples will help clarify how a trust works. I live in Ithaca, a small town in upstate New York and the home of Cornell University, where I teach. Ithaca sits at the southern tip of Cayuga Lake, one of eleven Finger Lakes. Rich farmland rises steeply from the shores of these lakes and rolls across the horizon, creating a landscape of undulating hills, deep gorges, and thundering waterfalls. It is a place of stunning natural beauty, which many people want to preserve for future generations. In 1989, a group came together to create the Finger Lakes Land Trust, whose mission is “to conserve forever the lands and waters of the Finger Lakes region, ensuring scenic vistas, clean water, local foods, and wild places for everyone.”

The trust fulfills its mission by acquiring land and creating a chain of nature preserves that are open to the public year-round. The trust owns the land and holds it for the benefit of the public. A board of directors oversees the trust, though a paid staff of professional managers and conservationists manages its day-to-day operation. People can contribute to the trust by donating land, either as a gift or as a bequest, or by contributing money or other assets, which the trustees can use to purchase additional land. To date, the trust has brought around 27,000 acres under its protection. This land cannot be purchased on the private market. No matter how much private investors offer, the trustees are not permitted to sell the land.

The urban counterpart to a conservation land trust is a community land trust. While the former acquires and decommodifies rural farmland and forests, the latter acquires and decommodifies urban property. Both hold the assets for the long-term benefit of another group—in the former case, the public; in the latter, the residents of a particular area. Both are overseen by a board of trustees, who follow a set of rules established at the creation of the trust, and both are managed by a professional staff. Community land trusts have existed for decades, and hundreds of successful models exist all across the country.

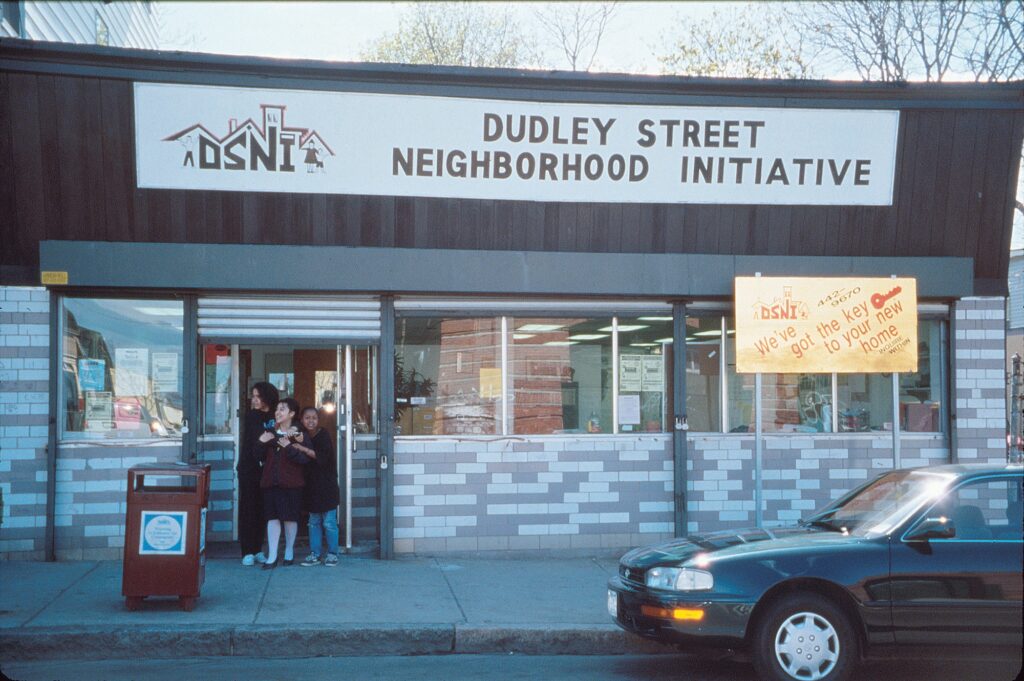

The oldest community land trust, created in 1969, is in Georgia; the largest is in Burlington, Vermont. The most famous, however, and the one whose operation provides a model for a distressed neighborhood like Olneyville, might be the Dudley Neighbors Incorporated land trust, in an area known as the Dudley Triangle in the Roxbury and Dorchester neighborhoods of Boston. As in Olneyville, the economic downturn of the1970s and ’80s devastated the triangle. Vacant lots became toxic dumps, and abandoned buildings burned to the ground. By 1984, after years of disinvestment and arson, nearly a third of the triangle’s land lay vacant. In the same year, a group of determined residents formed a nonprofit community group, later named the Dudley Street Neighborhood Initiative (DSNI), to organize and mobilize area residents against the illegal dumping and arson that beset the area.

When the City of Boston circulated a neighborhood redevelopment plan that included no input from Dudley residents, DSNI responded. Area residents researched and drafted a comprehensive alternative to the city plan. Under the rallying cry “Take a Stand, Own the Land!” residents settled on a community land trust as the best way to decommodify land to preserve its long-term affordability. To implement its plan, DSNI created Dudley Neighbors Incorporated (DNI), a community land trust. In 1988 Boston gave the land trust the power of eminent domain, which allowed the trust to acquire much of the privately owned but abandoned or vacant land within the triangle and incorporate it into the trust. The city also owned a great deal of vacant land in the triangle, which it transferred to the trust. Today the trust owns the land and buildings on this land for the benefit of the neighborhood’s residents.

Within the trust, DNI gradually developed the land as permanently affordable housing by decoupling it from the unrestrained forces of the market. Under an arrangement much like what the community development corporation ONE Neighborhood Builders uses in Olneyville, buyers who purchase a home built by DNI own the structure but not the land beneath it. This creates the classic quid pro quo of shared equity: because the homeowner does not own the land, she can buy the house at a considerably lower price. In exchange, she agrees to give up the right to sell for whatever price the market could demand. Instead, if she chooses to sell, she must sell to another eligible low-income buyer and cannot sell at the market rate.

As in Olneyville, these shared-equity arrangements have helped the Dudley neighborhood thrive by ensuring a stable supply of quality homes at below-market prices. They enable homeowners to resist displacement and give them a greater attachment to the neighborhood by reducing their financial incentive to sell. They also eliminate the risk that speculators with no commitment to the neighborhood will snatch up distressed homes and flip them at prices beyond the reach of the average neighborhood resident. Though land trusts typically focus on homeownership, their essential benefit is to decommodify land, which makes them equally appropriate for rental units. Most people living on land owned by a community land trust, in Dudley and across the country, rent rather than own. They live in multiunit buildings owned by the trusts, which rent units to residents at affordable rates. Land trusts can also decommodify commercial property, helping to ensure that businesses serving the needs of low-income residents will not be displaced by rising rents. Though DNI originally focused on affordable housing, it has gradually expanded. As of 2016, the trust managed 226 homes, an urban farm, a community greenhouse, several parks, and a town common.

Yet there is a critical difference between the shared-equity arrangement created by ONE Neighborhood and the arrangement created by DNI. In Olneyville, ONE Neighborhood owns the land; in the Dudley Triangle, the residents of the neighborhood collectively own the land. In Olneyville, the residents in shared-equity housing divide their wealth with ONE Neighborhood, an outside nonprofit; in the Dudley Triangle, they divide it with the rest of their neighbors. Increases in the land’s value accrue to the neighborhood as a whole rather than to an outside steward, however benevolent. Jennifer Hawkins, the current executive director at ONE Neighborhood and a passionate, dedicated advocate for Olneyville, understands this distinction. I once attended a meeting with Hawkins and other members of her staff and raised the idea of a community land trust. She nodded. “I don’t want to own Olneyville,” she said. She was speaking for the organization, of course, not for herself. Yet despite this preference, ONE Neighborhood remains one of the largest private land owners in Olneyville. It owns some of the most valuable residential space in the neighborhood. Increases in the value of the land accrue to ONE Neighborhood, not to residents, and ONE Neighborhood decides how the land will be developed and used. The welfare of the neighborhood continues to depend on the magnanimity of outsiders. This is neoliberal precarity in action.

The community land trust is an exceedingly important model for neighborhood well-being, and it has received a great deal of attention as a bulwark against gentrification and displacement. Yet it does not go far enough toward creating vibrant, sustainable low-income neighborhoods. To begin with, most land trusts are far too small to stabilize an entire neighborhood. They provide long-term affordable housing to the people living in houses and apartments owned by the trust, but that is not enough to protect the neighborhood from gentrification and displacement. Moreover, though land trusts decommodify property, the interconnected needs of a distressed neighborhood go well beyond preserving the affordability of land. In a neoliberal age, the government will not—and the private sector cannot—meet these interconnected needs. To fill the gap, neighborhoods like Olneyville must rely on the ecosystem of small nonprofit organizations, which run desperately important programs and services but operate on a shoestring. If these organizations close, the neighborhood becomes practically unlivable for the people who depend on them. Preserving these organizations, and bringing them within the stable ownership and control of neighborhood residents, is just as important as decommodifying land.

Many community land trusts (CLTs) have also set their sights too low. As the authors of one study found, the staff and leadership of CLTs often “do not challenge the larger relations, processes, or institutions of society.” Instead they see themselves as making it easier for low- income residents to survive in a neoliberal state that has left them behind. Like nonprofits in Olneyville and elsewhere, many CLTs are service providers rather than neighborhood activists. As laudable as that may be, it is not enough. As the retired pastor at St. Teresa’s Church in Olneyville, Father Raymond Tetrault, a legendary advocate for Latinx residents, understood many years ago, neighborhood residents must own and control their fate. Neighborhoods like Olneyville need a model that replenishes social capital, restores a sense of community, and gives its residents ownership and control of local resources, including but not limited to the land. That is the motivation behind the neighborhood trust.

Suppose we established a fund, held in trust by Olneyville residents for the long-term benefit of the neighborhood and its low-income residents; call it the Olneyville Neighborhood Trust. All the resources that flow into the neighborhood from philanthropies, foundations, community banks, and governments, which now go to nonprofits, would instead pass into and be administered by the trust. The trust would own and control these assets and would have a man- date to address the interconnected challenges that confront the neighborhood, but in a way that preserved sustainable affordability.

Beyond that broad mandate, the residents could tailor the trust’s terms and objectives to meet the unique needs of the neighborhood. As those needs changed, so could the terms of the trust, but only if the residents of the neighborhood agreed. A board of trustees would administer the trust, and a majority of the board would always come from the neighborhood and its trusted allies: the residents, business owners, and civic leaders who best understand the place and what it needs. They would be elected for rotating terms of office by their neighbors, giving the residents a direct voice in the direction of the trust and the disposition of its assets. This would restore the democratic accountability that is absent in the current model and make the trust an engine not simply of sustainable economic and neighborhood development but also of civic participation. As in any trust, the board could hire a professional staff to manage daily operations.

In time, a neighborhood trust would fill the gaps opened by neoliberalism and end the precarity it has created. To begin with, the trust could decommodify land by creating shared-equity arrangements in commercial and residential property, just as community land trusts do now. But a neighborhood trust would go substantially beyond this. It would give residents local ownership and control of the resources that flow into their neighborhood, liberating them from the steward- ship of outside nonprofits.

Not only is this important in its own right, but maintaining ownership and control encourages neighborhoods to develop and tap local residents’ expertise, thus building essential skills in self-governance and ending the dependency that too often defines the current model. That was the core insight of Father Tetrault’s work at Saint Teresa’s: placing power in the hands of the people affected by neighborhood problems builds leadership and self-sufficiency. Once the trust controlled these resources, residents could decide how they should be deployed. If, for instance, the people living in Olneyville believed that English for Action provided a more valuable service than some other organization in the neighborhood, they should be allowed to allocate their resources accordingly. That choice should not be made by an outside foundation. Organizations would thus be accountable to the neighborhood and the people who live there, rather than to a distant philanthropy. The neighborhood would be better off, since the needs and wants of low-income residents would be catered to directly.

In addition, a neighborhood trust could invest its resources to create an endowment—a trust fund—that would help it weather economic downturns, survive the inevitable shifts in priorities by funders, and create a sustainable, independent stream of income that might ultimately free the neighborhood from its dependency on outsiders. As the trust grew, it could use the leverage that comes with wealth—a leverage that the rich enjoy as a matter of course—to restore the safety net that neoliberalism has shredded. It could, for instance, pressure would-be employers who wanted to contract with businesses and organizations in the trust to hire local firms, pay a living wage, and provide childcare, health care, and retirement benefits for their employees. In addition, the trust could devote a small fraction of its resources to defray short-term costs to low-income residents and businesses, much like the old community chests that thrived in the first half of the twentieth century.

The greatest challenge for our neighborhood trust would be acquiring the land to bring it under resident control. In many locations, particularly those on the cusp of gentrification, even vacant and abandoned land may be far too expensive for the residents of a distressed neighborhood to acquire, as landowners simply hold on to the unused land in the hope that they can sell it when values go up. In Dudley, the DNI acquired most of its land by a combination of eminent domain and direct transfer from the city. Wherever municipalities own vacant and abandoned property, they should transfer it to the ownership and control of a properly organized neighborhood trust. In places where this is not possible, however, the inability to purchase land makes it difficult for the trust to achieve its full potential.

To meet this challenge, I would add another tool that distinguishes a neighborhood trust from a community land trust: increasing the funding for neighborhood trusts by creating a combination of federal and state tax credits. State and federal governments could give neighborhood trusts a tax credit that they could sell on the open market, much in the way developers sell Low-Income Housing Tax Credits. Eligibility for the tax credit would be limited to neighborhood trusts that meet certain criteria, such as accounting transparency, demonstrated engagement with and responsiveness to area residents, and enforceable rules against self-dealing by trustees.

Investors who purchased the credits would receive a guaranteed stream of income for a term of years, ideally several decades or longer. The trust would use the proceeds of the sale to fund its operations and build its endowment, deploying the money to meet the overlapping needs of a distressed neighborhood without sacrificing long-term affordability. But unlike with the Low-Income Housing Tax Credit, neither investors nor state, federal, or local governments would have any control over the trust or its assets. If, for instance, neighborhood residents decided the best use of the money was to create single-room-occupancy housing for the lowest-income residents—or those who were homeless—then investors and the government could not object. As long as the assets were not used to discriminate against a protected class—by excluding people based, for instance, on race, ethnicity, religion, gender, or sexual orientation—the trust would have complete control over its funds. Capital would grow, but people who have historically been marginalized and excluded would have control over the assets.

Though I believe tax credits are the ideal way to fund a neighborhood trust, they are not the only way. Cities have long used a host of tools to raise money for projects in low-income neighborhoods. Tax increment financing, for instance, allows a municipality to pool the property tax revenue generated within a designated district and use it to fund projects within the area. In addition, as community land trusts have gained popularity, supportive municipalities have begun to fund them in creative ways, including start-up grants, operating subsidies, and technical assistance. Private institutions like Citibank, in partnership with nonprofits dedicated to affordable housing, have also contributed funds to create or expand existing CLTs. All these tools should be used to fund neighborhood trusts. With any funding mechanism, however, the key condition, which must not be sacrificed, is that the poor must own and control the assets.

Nothing about a neighborhood trust would require neighborhood residents to break new organizational or legal ground. On the contrary, the trust would draw from established models, including community land trusts like DNI and nonprofit community development corporations like ONE Neighborhood Builders. Like DNI, the trust would acquire property and sell it only pursuant to a shared-equity arrangement. The rights reserved by the trust would be held in common by neighborhood residents and managed by the trustees. Like ONE Neighborhood, the trust would serve as a backbone organization for all funds that entered the neighborhood, distributing the resources and taking the lead in developing and maintaining relationships among the organizations that provided services within the neighborhood, some of which the trust itself could develop. By combining these two models, the neighborhood trust could develop a cradle-to-grave blanket of social services that tended to the overlapping and interconnected needs of low-income residents throughout their lives, while keeping the neighborhood affordable. And funding the blanket through tax credits uses a tool that is familiar to both lawmakers and investors.

In one respect, the neighborhood trust is the next stage in a long history of neighborhood development. It vests ownership and control with neighborhood residents rather than with outsiders, creates local expertise while building social capital and neighborhood wealth, and protects long-term affordability. By aligning capital with the poor rather than against them, the trust corrects the flaws of neoliberalism and allows a distressed neighborhood to raise itself from precarity without paving the way for displacement. In another respect, however, the neighborhood trust is the realization of a very old ambition. The current nonprofit sector came into existence more than a half century ago with the dream of giving low-income residents local ownership and control of neighborhood resources. But prior attempts have come to naught, and in today’s neoliberal age, local ownership and control seem like a fantasy. The goal of the neighborhood trust is to make that vision a reality.

Like any innovation, the neighborhood trust will meet with objections. Some, for instance, will complain that such a scheme is not radical enough. It takes neoliberalism as a given—as an unalterable background philosophy that writes the rules of the game—and merely tries to protect places like Olneyville from its toxic effects. Rather than call for neoliberalism to be ripped out by the roots, the trust deploys the tools of neoliberalism to fund its operations.

This is a fair criticism, and I would like nothing better than for neoliberalism to be replaced by a robust national commitment to the welfare of the poor. At a minimum, the federal government should get back in the business of building public housing. The national refusal to provide and care for the most vulnerable among us is obscene, especially since it is neoliberalism that has made inequality worse and swelled the ranks of the working poor. Yet in today’s political climate, the obscenity will not end anytime soon. As political scientist Sanford Schram observed in his 2015 book The Return of Ordinary Capitalism, “As much as people have good reasons to wish away neoliberalism,” it is “the new normal,” and “its pervasive influence must be taken into account in pushing for political change.” Likewise, as Eric Levitz recently argued in a review of historian Adam Tooze’s new book, Shutdown, even the pandemic, which has so plainly laid bare the lethal inadequacy of market fundamentalism, does not seem to have seriously weakened establishment attachment to neoliberal orthodoxy. In our neoliberal age, neighborhoods like Olneyville must do what they can to transform themselves. When solutions are at hand, there is no point in waiting for a savior that may never come.

Even if neoliberalism were to disappear, I would still encourage Olneyville to develop a neighborhood trust. The Economic Opportunity Act of 1964, which launched the war on poverty, called for “maximum feasible participation” by the poor. This philosophy, however, was quickly abandoned, and the poor became passive recipients of federal largesse overseen by others. Restoring robust and equitable government funding to neighborhoods like Olneyville is necessary but not sufficient; those funds must be owned and controlled by the residents of the neighborhood and should be held within a legally protected instrument that allows residents to resist the invasion of unrestrained capital.

Other concerns with the idea of neighborhood trusts are more substantial. Some will argue that shared-equity arrangements of the sort I have endorsed deprive low-income residents of what has historically been the surest path in this country to the accumulation of wealth: ownership of property. Because homeowners in a shared-equity agreement do not own the plot of earth beneath them, when they sell their homes, they miss out on the windfall that can result from dramatic increases in the value of land. Losing the chance for this individual wealth is no small thing.

This argument is made even more urgent when we recognize that access to this wealth has never been color-blind. Blacks and Latinos have systematically been denied access to mortgages and ownership in areas where property values were increasing, so that they were far less likely to reap the financial benefit of homeownership. White homeowners have been able to live in these areas, and they have relied on this increase to fund a more privileged lifestyle. A large percentage of the wealth gap between whites and Blacks is the result of this differential access to homeownership. How can we justify a financial instrument like a neighborhood trust that perpetuates this inequity? Why shouldn’t people of color have the same opportunity for homeownership as whites?

This argument has great moral and economic force, but it is ultimately not a good reason to reject a neighborhood trust. To begin with, as Keeanga-Yamahtta Taylor has argued both in her 2019 book, Race for Profit, and in these pages, claims about the economic power of home ownership mistakenly assume “that all people enter the housing market on an equal basis or that the housing market itself is a neutral arbiter of value.” Because neither assumption is warranted, the value of ownership by the poor must be discounted by the cost of systemic racism. In any case, the existence of a neighborhood trust does not prevent a qualified purchaser from buying any home she can afford, including one on the open market rather than one in the trust. Furthermore, homes in the trust are available only to people who could not have afforded a home at market rates. Without shared equity, they are priced out of ownership entirely, at least in Olneyville. The trust allows them to enter and remain in a neighborhood that would otherwise quickly become unaffordable. In that way, the trust increases the number of low-income residents who can become homeowners in desirable places, even if they lack the full bundle of rights enjoyed by residents who can buy a home outright. And of course, the trust allows homeowners to build a credit history so that they can qualify for a conventional mortgage and later purchase a home on the open market, should they desire.

Third, the argument against shared equity misses the point of the trust, which is to maintain the long-term affordability of the neighborhood as a whole. The trust protects the shared wealth of the neighborhood by stepping away from our obsessive focus on individual profit. The person who buys a home in the trust makes a commitment to sustaining a thriving, diverse, and affordable neighborhood. In exchange for that commitment, she relinquishes the right to cash in on gentrification, which would make her home unaffordable to the next generation of low-income buyers. The trust is an investment in the neighborhood at the expense of the individual. People who want to make that investment and be part of such a community will pay the economic price, and those who do not are free to buy elsewhere.

Finally, the flexibility of the trust rules means that the terms of the shared-equity arrangement can be adapted to fit the neighborhood’s changing needs. The neighborhood may decide, for instance, to alter the terms of the trust by allowing homeowners to purchase full ownership rights from the trust at a below-market rate or acquire them outright after a certain period of uninterrupted residency—say, fifteen or twenty years. All these options can be written into the trust agreement. An incentive for long-term residency would encourage the owner to stay in the neighborhood, maintain the house at a high level, and contribute to the neighborhood so as to increase the value of her investment. The residents in one neighborhood may want to write its trust rules to eliminate the opportunity for the owner to acquire the land rights; in another neighborhood, the residents may want to provide such an opportunity after twenty years; in another, after ten. If a neighborhood wants, it can even vote the trust out of existence and liquidate its assets. Like the neighborhood it protects, the trust can last forever, but it can also have a life span. As with everything else, the decision should be left to the residents.

Another potential objection to neighborhood trusts is that developing a sizable endowment will take years, particularly if the federal government does not use a tool like tax credits to encourage capital to invest in the neighborhood trust. This is undoubtedly true, which is why I do not see the trust replacing the current approach right away. In the immediate term, money would continue to flow into the neighborhood from outside funders like philanthropies, foundations, community banks, and the government. But the funding should be owned and controlled by the neighborhood trust, rather than the nonprofits. The trust could use the resources to fund nonprofits and to operate the same sorts of initiatives and organizations that currently exist. In short, life with a neighborhood trust may at first look a great deal like life without it. Over time, however, the trust will grow in assets and importance, until eventually neighborhoods will no longer have to rely on outside funders to remain affordable to residents of limited means.

Still others will claim that a neighborhood trust merely replaces a diverse set of small, specialized nonprofits with a single large non-profit. Yet a neighborhood trust does not merely create an extra layer of bureaucracy. It gives residents ownership and control over the resources that flow into their neighborhood—a power they do not presently have—and exercising that power is vital. Residents will have to decide democratically who is eligible to vote and serve on the trust. They may allow all neighborhood residents to vote, or they could limit voting to residents who have lived in the neighborhood for a particular length of time. They may create a board position for one or two nonresident allies, so that people like Frank Shea or Jennifer Hawkins could serve. Or they might restrict membership to low-income residents. But this complexity is a benefit, not a drawback, since these decisions are inherent in self-government. The capacity for, and attachment to, civic participation that a trust engenders would carry over to other aspects of community life. Residents who are engaged in the ownership and control of their neighborhood are more likely to be engaged in their city, state, and country. Creating and operating a neighborhood trust would increase self-governance.

Close attention to the inherent value of self-governance also helps us respond to a different objection. Some will say, quite rightly, that a neighborhood does not speak with a single voice. Though Olneyville is predominately low-income and Latino, great racial, ethnic, and class diversity nonetheless exists in the neighborhood. It is certainly wrong—and more than a little insulting—to expect that all Olneyville residents have the same view on issues like policing, housing, charter schools, and so on. Given this diversity, it is entirely possible that a majority of low-income residents in Olneyville would not want a neighborhood trust. Indeed, they may prefer to retain the current model. I fully accept this possibility. The point, however, is that the poor should be able to make their own choices. What they choose does not matter as long as the choice is theirs, expressed in free and fair balloting. Anything else is at best paternalistic.

Another objection concerns the availability of land. Some cities are now so densely built that practically no land exists that a trust could acquire, even with funds from a tax credit. I grant that in some locations, the tsunami of unrestrained capital has raised the cost of land so much that there is no longer any point in talking about maintaining affordability for low-income residents. But those neighborhoods are not the ones we are trying to preserve. In those places, capital has already thoroughly displaced the great majority of low- income residents, and we can have little hope of bringing them back. The neighborhood trust is meant for low-income neighborhoods that can still be preserved, and in those places, land is still available. As the Lincoln Institute of Land Policy reported in 2018, vacancies remain at “epidemic levels” in our older industrial cities. In 2017, for instance, Detroit had over 120,000 vacant lots. To put it mildly, where a neighborhood trust is most needed, a want of land is not the problem.

This leads to a final objection, perhaps the most insidious: the notion that residents of distressed neighborhoods simply are not up to managing their own affairs. They lack the skills needed to oversee a trust and its endowment, and they cannot do the job of the many nonprofit organizations that currently provide vital services to places like Olneyville. The poor, goes the argument, need better-educated, better-placed outsiders to do this work for them. Exactly this kind of paternalism, in fact, is what I heard when I presented my research to members of the Olneyville Collaborative: “Great idea, but they’re just not ready.”

I disagree, strongly. To begin with, by treating the residents of a low-income neighborhood as part of the problem rather than part of the solution, this objection exposes the stewardship mentality of the current approach. Many people need training when they start a job, and if low-income residents of a distressed neighborhood lack skills, they can certainly acquire them. In addition, those who level this objection seem to suppose that an employee must be qualified to fill every position in an organization. That is not remotely true. Like anyone else, residents of a distressed neighborhood can hire advisers and outside experts and make informed judgments based on their input. They can also retain much of the staff that currently works in the nonprofits throughout the neighborhood. The key point is that these choices should be left to low-income residents rather than to outsiders.

More importantly, when I hear such objections, I cannot help but think of the long history of neighborhoods like Olneyville. Even if we assume the people who live there cannot manage their own affairs—an assumption I very much reject—that deficit was caused in no small measure by two generations of neglect and mismanagement by people with greater resources and power. We cannot in good conscience create a system that impoverishes a neighborhood, and then point to neighborhood poverty as an excuse to keep the system in place. The history of distressed neighborhoods like Olneyville offers a powerful argument in favor of local control, not against it. In any case, the great success of community land trusts across the country, including Dudley Neighbors Incorporated, suggests that any supposed skill deficits within distressed neighborhoods are more imagined than real, and certainly not irreversible.

At the end of the day, the current approach to neighborhood wellbeing will not protect places like Olneyville. The poor need to own the resources that flow into their neighborhood, and they need defenses to protect them from footloose capital. This means removing assets from individual hands and placing them in the shared hands of neighborhood residents, who hold those assets in trust for the benefit of the group and insulate them from private profit making and political manipulation. In an age when the failure of unregulated capitalism is becoming more evident every day, we cannot implement options like the neighborhood trust quickly enough.

Editors’ Note: This essay is adapted from Thanks for Everything (Now Get Out) by Joseph Margulies © 2021. Excerpted with permission from Yale University Press.