Last month, U.C. Berkeley economist Emmanuel Saez spoke to the Center for Ethics in Society at Stanford University about his pioneering research into global income inequality. A critical question his work raises is whether high taxes on the wealthy can curb inequality. Before his talk, Saez sat down with Stanford sociologist David Grusky to discuss further why taxation, though a blunt instrument, might be the best available solution.

That said, I suspect that there are some features of your work that you think have been misunderstood or, at the least, inadequately addressed in current debates about inequality. Could you talk a bit about this underappreciated side of your work?

Emmanuel Saez: I did this key work on income concentration in the United States with my colleague Thomas Piketty, and we were indeed quite surprised by how successful our research has been in the public debate. Initially this was really academic work building on the long tradition of the famous economist Simon Kuznets, who started the data series back in the 1950s. So we never approached it in a way that would necessarily be easy for the broader public and the press to use. We had to adjust over time to try to talk to the public and present our findings in a way that was the simplest, because we’ve discovered that to have an impact in the broader world, the way you present your research—the design, the framing—has a tremendous impact.

Naturally the public has focused mostly on the very recent period. But the key goal of our study was to show a very long perspective—a century long perspective—and to think about long-term changes rather than year-to-year changes. And I think there’s a lot to learn about how those long-term changes are related to policy making and government action.

DG: I’m prompted by your last point to suggest that another underappreciated feature of your work is that it delivers rather provocative hints about the causes of the increase in inequality. That is, it not only lays out the descriptive trajectory of income inequality, but also suggests what’s driving that descriptive trajectory.

We participated in a Boston Review debate on one account of the sources of the recent takeoff, namely the expansion of rent, where rent is understood as sweetheart deals, corruption, backdating stock option contracts—all sorts of pay-setting practices that permit those at the top to secure more than they would in a competitive market. On the basis of your research, do you think that rent is an important source of the recent growth in income inequality?

ES: If we define rent in terms of situations where pay doesn’t correspond to what economists call ‘marginal productivity’—that is, the economic contribution a person is providing—I would say yes, because the evolution of income concentration over time and across countries has a number of features that are inconsistent with the story where pay is everywhere equal to productivity. The changes in income concentration are just too abrupt and too closely correlated with policy developments for the standard story about pay equaling productivity to hold everywhere. That is, if pay is equal to productivity, you would think that deep economic changes in skills would evolve slowly and make a gradual difference in the distribution—but what we see in the data are very abrupt changes. Basically all western countries had very high levels of income concentration up to the first decades of the 20th century and then income concentration fell dramatically in most western countries following the historical narrative of each country. For example, in the United States the Great Depression followed by the New Deal and then World War II. And I could go on with other countries. Symmetrically, the reversal—that is, the surge in income concentration in some but not all countries—follows political developments closely. You see the highest increases in income concentration in countries such as the United States and the United Kingdom, following precisely what has been called the Reagan and Thatcher revolutions: deregulation, cuts in top tax rates, and policy changes that favored upper-income brackets. You don’t see nearly as much of an increase in income concentration in countries such as Japan, Germany, or France, which haven’t gone through such sharp, drastic policy changes.

DG: There are a few other features of your work that appear consistent with a rent narrative. For example, you’ve shown that income growth among the top 1 percent often comes at the expense of incomes at the bottom of the distribution. Hence there’s a zero-sum character to the distribution that appears consistent with a rent theory. And you’ve also shown that reducing the marginal tax rate may help the 1 percent but doesn’t appear to lead to overall GDP growth, a result that is again consistent with a rent formulation. Do you think those two features of your work offer further supporting evidence for an account based on rent?

Tax policy is a blunt instrument, but it works.

ES: Yes. There have been a key number of policy developments, especially cuts on top tax rates in a number of countries, that have led to a surge in pre-tax top incomes in those countries, the best example again being the United States and the United Kingdom. All the data we’ve gathered from so many countries over so many years tells you that, indeed, the level of top tax rates plays a large role in pre-tax income concentration. The key question is, what is the mechanism that leads higher or lower top tax rates to lower or higher top incomes?

The standard story among economists is that if those in the top bracket earn more that’s because they are working more and contributing more to the economic pie. So in that scenario, reducing top tax rates and having higher incomes at the top would be a good thing. However, if that were the case, the growth in top incomes should not come at the expense of lower incomes and it should stimulate economic growth. The difficulty, however, is that if you look at the data you don’t see clear evidence that countries who cut their top tax rates and experienced a surge of top incomes did experience overall better economic growth.

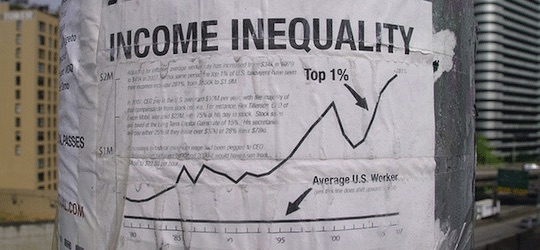

An alarming fact in the United States concerns the patterns of economic growth of the top 1 percent versus the bottom 99 percent. We know that in the long run economic growth leaves all incomes growing. If you take as a century long picture, from 1913 to present, incomes for all have grown by a factor of four. But then when you look within that century of economic growth, the times at which the two groups were growing are strikingly different. From the end of the Great Depression to the 1970s, it’s a period of high economic growth, where actually the bottom 99 percent of incomes are growing fast while the top 1 percent incomes are growing slowly. It’s not a good period for income growth at the top of the distribution. It turns out that that’s the period when the top tax rates are very high and there are strong regulations in the economy. In contrast, if you look at the period from the late ’70s to the present, it’s the reverse. That’s a period when the bottom 99 percent incomes are actually growing very slowly and the top 1 percent incomes are growing very fast. That’s exactly the period where the top tax rates come down sharply. So, of course this doesn’t prove the rent-seeking scenario but it is more consistent with it than with the standard narrative.

DG: It seems that you and I agree that, in explaining what’s driving the recent divergence in the income distribution, we should turn at least in part to a rent narrative. Where we may differ somewhat—and I’d like now to explore our differences—is on the matter of what policies might be adopted to address that portion of the increase in inequality that’s attributable to rent. Insofar as there were no rent involved in the takeoff in inequality, many people would argue that the takeoff is unproblematic, and indeed may even be all for the good. But insofar as some of that rise is attributable to rent and cannot be understood in terms of rising marginal productivity at the top, we might regard it as inequality that should be curtailed. So then the policy question comes to the fore.

In the Boston Review piece, I suggested that, if there are institutional practices in play that generate rent, we should reform those practices and cut off rent seeking at its source. It’s strange indeed, I argued, that the antidote to which most people reflexively move is tax policy. This move is tantamount to saying “just let rent happen, there’s nothing we can do about rent itself, all we can do is accept it and then tax some of it away.” It seems on the face of it rather more attractive to look to the source in addressing rent. And you responded, “Not so fast.” Why do you think tax policy might be a better way to address rent?

ES: The first answer is that we have a historical record, and tax policy has been a tried instrument. If we had had that conversation a century ago, when no country had started really steep progressive taxation, you might legitimately have told me, “You are making a theoretical case. How can I trust you are not going to break the economy?” But we’ve seen all major western countries go through periods of very high taxation of top incomes that have indeed reduced deep concentration of pre-tax income without hurting economic growth.

The world of course has evolved. There is more globalization, mobility of capital, and mobility of people across countries for tax reasons could be a concern. I’m not saying it’s as easy as it was in the past, but at least I have a solid record to return to when I suggest that tax policy is the solution.

Now, it’s true that tax policy is a blunt instrument, because it is going to tax all high incomes and rent might differ quite a bit across high incomes. That is, some high incomes probably do reflect true marginal productivity; the example that is most often pointed out are sportsmen who generate great economic value because there is so much public interest in seeing them perform. Other forms of high income started with real production. Think about Microsoft, Google, and Facebook: they really invented new products, but after a while they really have become entrenched—a semi-monopoly. It’s a monopoly because they’ve captured an enormous fraction of the market and they’ve started earning rents based on the products they’ve developed. And then there are some CEOs who have engaged in corrupt practices. But when you tell me we are going to combat rent on a case-by-case basis, I don’t have historical examples showing me that this is going to work as well as taxation. For monopoly there’s the anti-trust policies, and that’s a good and important one. For CEO pay, I think the historical record has been pretty bad for those who think we can regulate the practice. For example, Clinton in 1993 limited the deductibility of top executive pay for corporate tax purposes to $1 million per person unless the pay was tied to performance. That meant that stock options and bonuses were excluded from that $1 million. And what you saw then was a surge in this form of pay. Another example is what happened with the corporate scandals a decade ago, such as Enron and Worldcom. CEO and executive practices were really corrupt and discussed a lot in the press led to some new regulations. But now you look at the data and it doesn’t seem that those regulations have had a strong impact on CEO pay.

So I don’t oppose fixing rents systematically, but you have to come to me and give me examples of why you think certain policies are going to work. Tax policy is blunt, but it works.

There has to be a dramatic historical event that allows a country to shift gears and change its tax policy.

DG: I confess to the conceit that, despite all the failed reform of the past, we can yet get it right. That said, I think you just gave a very compelling account of how difficult it is to cut rents off at their source, how our best laid plans oft go awry. We simply can’t foresee all the ways in which institutional reform can be manipulated. It’s a difficult task; I understand that. But let me ask you to explain exactly why tax policy can lead to changes in rent-seeking at the very top. That is, if I understand your argument, it suggests that whenever there are relatively high tax rates at the top a CEO might be less inclined, for example, to pack the board of directors with cronies who would support high compensation. This is because our forward-looking CEO appreciates that much of the additional compensation would simply go right back to the government. Is that the main mechanism through which you think tax policy works?

ES: Yes, for rent-seeking in terms of excess compensation, I would think that’s likely to be the main mechanism. The other aspect is capital income—the creation and perpetuation of large fortunes. And there again we have good evidence from the historical record: very progressive taxation definitely erodes the ability of those who have accumulated large fortunes to perpetuate those wealth holdings.

The striking fact is that no matter what the mechanism is, what we observe empirically is that in countries that have really steep progressive taxation, you don’t observe sustained high levels of income concentration. So some mechanism must be at work reducing pre-tax incomes.

DG: I think a lot of people would be worried that, by resorting to tax policy, you reduce not just the incentive for rent-seeking but also the incentive for undertaking the hard work that makes for real productivity. This may well be a big price to pay. How do you make sense of that dilemma?

ES: It is a central question and indeed economists have expended a lot of effort trying to understand the relationship between the rewards of working and behavior. Do taxes and transfers that reduce the reward for working discourage work? There are many situations where reducing the reward to work leads to less work. That’s true for the bottom of the distribution, especially for parents with kids who have very high opportunity costs for work. And that’s true for people near retirement as well: it’s been shown that if you reduce the reward to working through the retirement system you can easily have effects on the retirement margin.

For top earners, we need more research, but I have yet to see a study that shows me that when you increase top tax rates, top earners work less. An interesting study that was done by Robert Moffitt and Mark Wilhelm using the tax overhaul of 1986—Reagan’s big second tax reform. The study showed that when Reagan cut the top tax rate, pre-tax top income surged, but the authors looked at the hours of work of those high earners and couldn’t see any effect on their reported hours. Of course, it was a small sample, but I hope that in the future, researchers can look at margins like retirement—do highly paid executives retire earlier now that Obama has raised their tax rates? That’s exactly the type of study we need. And of course I would revise my views if you showed me convincingly that those top guys are indeed working a lot less.

DG: Let me turn to some of the evidence that I think informs your view on this issue. What you found is that, when top tax rates go down, the top 1 percent garners an increasing share of pre-tax income. My query is whether that’s a causal relationship or a spurious one. It may be spurious because those countries that reduced tax rates at the top often happen to be the very same countries that allowed for institutional changes, such as de-unionization, that restricted the capacity of those at the bottom of the distribution to secure higher wages. And so it’s possible that the decline in the income share going to the top is actually driven, in part, by what happens at the bottom.

ES: I am sympathetic to this argument. It’s true that the Reagan and Thatcher revolutions were not only about reducing top tax rates; there were a number of other policies, such as deregulation and restrictions on unions. My best answer to you is that we have to do more data analysis. That is what I’ve prepared for my preparation this afternoon. I really look only at top tax rates but in principle you can use other variables like unionization, strikes, financial deregulations, etc., and then try to tease out the role of each factor. My sense, at this stage, is that it’s work we should be doing. The tightness of the correlation between top tax rates and pre-tax top incomes is so strong that I doubt that it will go away entirely. Maybe it will be not as strong but my guess is that a lot will survive.

Another reverse causal relationship that people mention is that if top earners earn more, they have more resources to deploy to influence policy makers through lobbying and campaign contributions. Once you have a very high level of income concentration, it might indeed be harder for policy makers to advocate and enact policies that are unfavorable to top earners.

So let me say this because I think it’s important: in the historical record we’ve seen, there always has to be a dramatic historical event—an economic crisis, a war, or something similarly dramatic—that allows a country to suddenly shift gears and drastically change its tax policy.

DG: This leads us to the matter of predicting the future. I can’t imagine anyone better positioned than you to assess where we’re likely going. And one could posit, off the cuff, three possibilities: the first is that the increase in income inequality, particularly the share going to the top 1 percent, will continue on unabated and ultimately take us to unprecedented levels of inequality, levels even exceeding what obtained in the 1920s; another possibility is that the increase will finally level off and we’ll remain at the current very high level for the foreseeable future; and a third possibility is that the Great Recession will, just like the Great Depression, usher in major policy and institutional changes that then lead to a compression of incomes. Which of those three possibilities strikes you as the most likely?

ES: Starting from the third scenario—yes, I think the Great Recession could have been this event. In the end, though, it probably won’t be. In part, it’s an effect of timing. In some sense, Obama was elected a little bit too early. Roosevelt was elected in 1932, at the end of the Great Depression. Obama, by contrast, was elected right when the Great Recession was happening and I don’t think he came prepared or with a strong will to address income concentration. As a result, even in the two years where he had quite a bit of power he didn’t do much about tax policy for top incomes. He punted, really. Now I believe his thinking has changed, but the political situation is different—it’s much harder to push for higher top tax rates given the layout of Congress.

That being said, the increase in top tax rates that was passed with the health care surcharge on top incomes, plus the increase in top tax rates back to the Clinton level is not negligible. It’s small relative to the changes that happened during the New Deal, but I wouldn’t say it’s zero. It’s a medium to small size change that in my view is not going to dramatically lead to a deconcentration of pre-tax income. So I think that the high level of income concentration we’re experiencing is likely to continue. And a dramatic change would happen only if the public really became convinced that it’s an unfair economic system, that a lot of that economic concentration is due to rents and those rents come at the expense of the rest of the population. But before the public is really convinced of that fact, I don’t think that you will see a dramatic policy change.

DG: This suggests the following history-is-perverse narrative: Because Obama was acting with knowledge of what transpired during the Great Depression, he was more likely to turn quickly to stimulus, a stimulus that proved just large enough to forestall a depression. But here’s the rub: Had Obama ignored the lessons of history, had he opted against stimulus, we might have had precisely that economic disaster that would have then precipitated more fundamental institutional reform. In that sense, knowing what happened in the Great Depression undercut the crisis and, ironically, ruled out any possibility of institutional reform of the sort that occurred in the New Deal. What do you make of that counterfactual? [laughter]

ES: I think I agree with this. If you look at the economic team that Obama assembled in his first administration, their preoccupations were “How do we stabilize the financial system?” and “How do we stimulate the economy using lessons from Keynesian economics that weren’t there at the time of the Great Depression?” Income concentration was not on their radar map. That’s why they were happy to extend all tax cuts, including tax cuts for the rich, because it didn’t strike them as that big an issue.